Tax nexus can create state tax filing obligations long before business owners realize it. Learn how nexus works, why it matters, and the common mistakes that lead to unexpected tax bills.

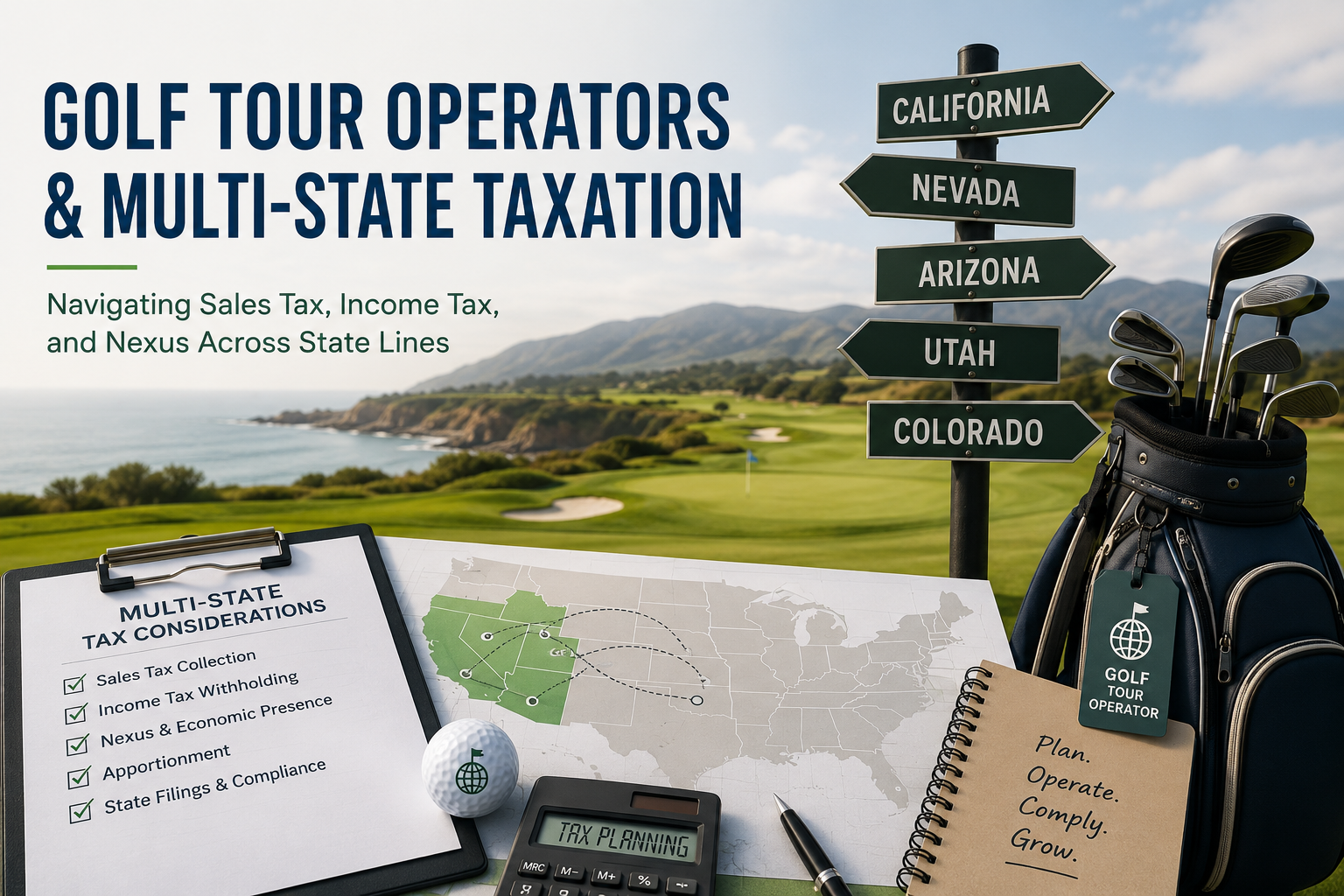

Golf tour operators often create tax obligations in multiple states without realizing it. Learn the key multi-state filing risks, nexus rules, and tax planning strategies every tour operator should know.

Golf course owners may be sitting on significant missed tax deductions. Learn how a cost segregation study can help recover prior-year depreciation and improve cash flow without amending past returns.

Many golf courses leave valuable tax deductions on the table every year. Learn the most commonly missed tax-saving opportunities and proactive planning strategies for golf course owners.

Golf courses rely on a network of vendors, tour operators, pro shops, and service providers. Learn why tracking margins is critical for profitability and long-term growth.

Discover how golf courses can use data analytics, technology, and modern management tools to improve profitability, increase member engagement, and make better business decisions.

Learn what restaurant prime cost is, how to calculate it, ideal target ranges, and why monitoring it is critical to restaurant profitability and long-term success.

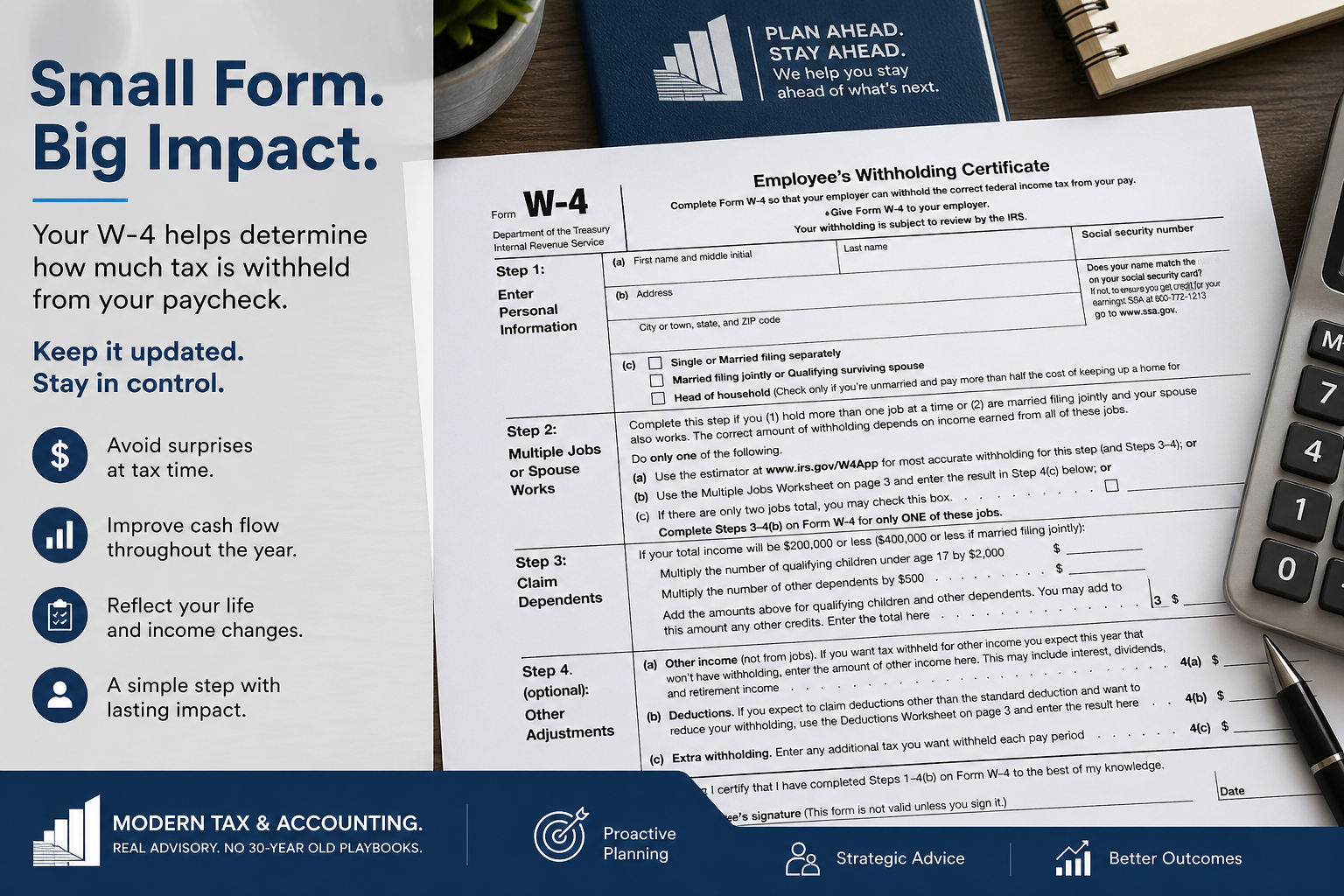

Not sure if your paycheck withholding is right? Learn why updating your W-4 matters, when to do it, and how to fill it out correctly to avoid surprises at tax time.

Accurate bookkeeping isn’t just about clean records — it drives better tax strategy, cash flow, and decisions. Learn why your CPA should be part of the process.